Rising interest rates have roiled stock and bond markets this year. But they’re also raising concerns about the outlook for the U.S. housing market, which has been a bright spot in the post-COVID economy. Having just sold and bought a home, I can understand individuals’ concern.

The average rate for a 30-year fixed mortgage loan, the most-common loan term, hit a 14-year high of5.8%last week. For better or worse, housing is one of the most rate-sensitive areas of the economy. Over the last couple years, ultra-low mortgage rates have been a boon to the housing market, stoking demand and pushingmedian sales pricesto new records.

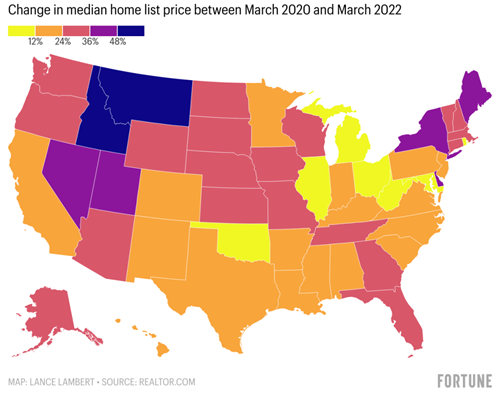

How Much Home Prices Are Up Since the Onset of the COVID-19 Crisis

Source: Fortune, Lance Lambert, and Realtor.com

So, where does the housing market go from here?

Higher rates mean higher monthly payments for buyers or homeowners refinancing mortgages. As the cost of buying climbs, demand typically cools, and prices soften. We’re seeing signs that demand is cooling because of sharply higher mortgage rates combined with high home prices:

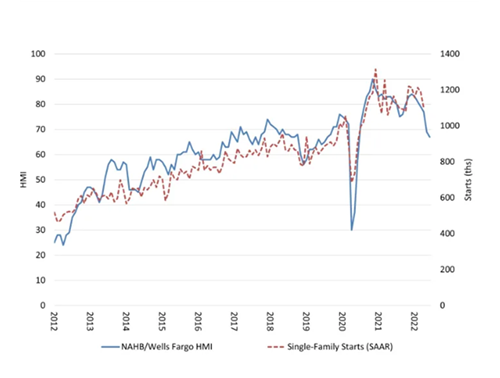

- Homebuilder optimism slumped in June, as did housing sales expectations, according to the National Association of Home Builders (NAHB). Traffic of prospective buyershas declined considerablysince March.

- Existing home sales fell for the third straight month in April. Sales were down 2.4% from the prior month and 5.9% from one year ago, according to the National Association of Realtors. (NAR) The median existing-home sales price increased at a slower year-over-year pace of 14.8% to $391,200.

NAHB/Wells Fargo Housing Market Index (as of June 15, 2022)

Source: Kestra Investment Management, National Association of Home Builders.

What has pushed up mortgage rates?

- The Federal Reserve doesn’t set mortgage rates, but it can influence them. The primary way the Fed does so is by increasing or decreasing the fed funds rate, which determines what rates are charged to banks for an overnight loan. Often when overnight rates are increasing, then long-term mortgage rates will also rise, but not always.

- The Fed can also influence mortgage rates by participating in themortgage-backed securities (MBS) market. After the outbreak of Covid-19 and other crises, the Fed spent billions to buy mortgage-backed securities and other bonds to improve market functioning and increase the money supply in the economy.

- Quantitative easing, as the policy is known, helped push rates to record lows. Now, as the Fed tries to fight inflation, that process is being unwound. The Federal Reserve has shifted from buying bonds to selling them — a process, known as quantitative tightening, that could put upward pressure on rates. Long-term rates are also influenced by expectations of long-term economic growth, inflation and the credit risk of mortgage borrowers.

Despite today’s higher rates, the housing market still faces shortages:

- Housing demand may be waning, but existing buyers must still compete for a low supply of available homes. That’s because builders have been stymied by supply-chain problems, labor shortages, a dearth of developable land, not to mention decades of underbuilding.

- In April, the inventory of existing single-family homes on the market was equivalent to just 2.2 months of supply, according to NAR. At the then-current sales pace, it would take only about two months for inventory to be fully depleted.

- Demographic shifts should bolster demand for years to come. Millennials, now America’s largest generation, are tiptoeing into marriage and homeownership. They are reportedlythe fastest-growing segment of homebuyers, accounting for 37% of buyers in 2020.

Supply of Existing Single-Family Homes for Sale (as of June 17, 2022)

Forward looking estimates may not come to pass. Past performance is no guarantee of future results. Source: Kestra Investment Management, FactSet.

With home prices at lofty levels, mortgage rates sharply higher and demand cooling, what are the chances that we’re headed for a 2008-style crash?

- The housing market certainly faces risks, from the high prices that make buying a homeunaffordable for many Americanstothe recent influx of institutional buyers, who may be less willing than individual homeowners to hold on to properties through thick and thin.

- But we don’t see the kind of systemic risks that led to the housing bust of 2008, such as a boom in subprime mortgages and complex financial instruments that encouraged such risky lending.

- In recent years, the bulk of new mortgages have been issued to high-quality buyers (those with credit scores exceeding 760), according to data from the New York Federal Reserve.

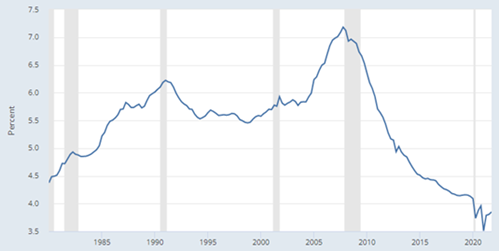

- Total mortgage debtis higher than it was before the 2008 crash. But Americansaren’t stretched nearly as thinwhen it comes to the percentage of their disposable income going to mortgage payments. In fact, mortgage payments as a percent of consumers’ disposable income is just 3.8%, near a record low and half of what it was before the 2008 crash.

Mortgage Debt Service Payments as % of Disposable Income

Source: Board of Governors of the Federal Reserve System, St. Louis Fed

To be sure, today’s higher rates are already taking some of the momentum out of what has been a frenetic housing market. But provided the economy doesn’t tip into recession and the labor market remains healthy, a soft landing seems like a more-likely scenario than a crash.

As someone who spends her days investing, it’s hard not to think about the investment implications of the house I live in. Then I turn off CNBC, sit down for dinner with my kids and husband, and remind myself that I live in a home. While my home’s price is important, the real value I get from it is time with my family.

Until next time, invest wisely and live richly.